Investor Brief

Strategic assets, not commodities.

Rare earths sit at the centre of global supply chains for energy, defence and advanced manufacturing. For investors, the East African chapter of that story is less about geology in isolation and more about strategic value, supply security and long-term upside.

Why They Matter

The magnet basket the energy transition cannot replace.

Neodymium, praseodymium, dysprosium and terbium drive the permanent magnets at the heart of electric drivetrains, wind turbines, precision electronics and modern defence systems. Their magnetic and conductive properties are difficult to substitute, which is what gives long-term demand its hard floor.

Governments across Europe, North America and Asia are openly working to secure alternative supplies. That policy backdrop creates an unusually constructive window for credible projects outside the dominant producing regions, and East Africa is one of the few places where new, sizeable deposits are entering serious evaluation.

Three Pillars

How the opportunity stands up.

01

Demand Growth

Electric mobility, wind generation, robotics and consumer electronics each lean on permanent magnets. The magnet basket, neodymium, praseodymium, dysprosium, terbium, is what gives the long-term price outlook its floor.

02

Supply Concentration

Global production sits with a small group of nations. Advanced-stage projects outside that group remain rare, and serious buyers in Europe, Japan and North America are openly looking for alternatives.

03

Strategic Positioning

Early-stage exposure carries the steepest re-rating potential: resource definition, drilling milestones, feasibility work, and the partnerships that connect a deposit to a downstream processor or end user.

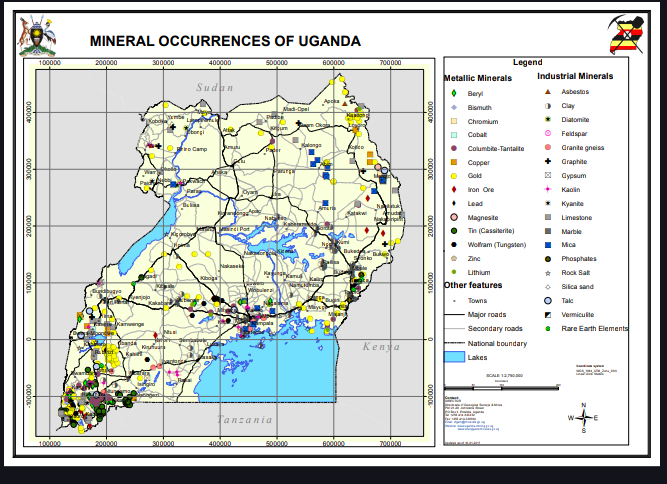

Uganda · Mineral Map

A landscape mapped, but not yet priced in.

The Ugandan mineral picture is unusually broad: metallic and industrial minerals across most regions, with rare earth occurrences confirmed in the south-east, the Rwenzori belt and along the western rift. The map is public. The interpretation, the licence status and the operator quality behind each marker are not.

That gap between what is mapped and what is understood by capital is the work.

Exploration Stage

Where the steepest re-rating sits.

Resource Discovery

Defining a commercially viable deposit through staged drilling and assay work.

Asset Appreciation

Valuation steps up through resource estimates, scoping studies and feasibility milestones.

Exit Pathways

Acquisition by majors, strategic partners or offtake-linked investors as a project matures.

Exploration outcomes turn on four things: the quality of the geological dataset, the deposit type, carbonatite, ion-adsorption clay, hard-rock, the infrastructure within reach, and the stability of the licensing regime above it.

The Clay Angle

Ion-adsorption clays and the case for a cleaner extraction pathway.

A meaningful share of the East African opportunity sits in weathered, clay-hosted deposits rather than hard rock. The economics are different: no crushing, no cracking, lower energy intensity, and a direct route to a rare earth carbonate that is ready for downstream separation and refining.

These deposits also tend to be broad and shallow. Drilling defines extent quickly, and projects can scale from pilot to production without the capital wall of a conventional underground mine. The Ugandan ion-adsorption story, anchored by the Makuutu corridor, is the clearest expression of that thesis in the region.

The Core Basket

Where the value concentrates.

Nd

Neodymium

Pr

Praseodymium

Dy

Dysprosium

Tb

Terbium

Gd

Gadolinium

A full rare earth basket carries fifteen-plus elements, but value concentrates in this magnet group. Strong projects tend to be priced against their share of these five rather than total tonnage.

Risk Picture

What a serious read does not skip over.

Processing Complexity

Separation of individual oxides is technical and capital-hungry. Projects with a cleaner extraction pathway carry a structural advantage.

Environmental Scrutiny

Tailings, water and rehabilitation are now front-of-mind for regulators and buyers. Compliance posture is part of the asset's value.

Market Volatility

Prices respond to geopolitics and policy as much as to fundamentals. Position sizing and time horizon matter.

Capital Intensity

The path from licence to production is measured in years, not quarters. Patient capital is rewarded; rushed capital rarely is.

Investor Positioning

A long-term strategic play, not a short-term trade.

The right framing for capital entering East African rare earths is participation in a critical-minerals supply chain that the global economy is actively rebuilding. The projects worth backing share a recognisable shape: a credible technical team, clear licensing, a defined roadmap from exploration to resource to development to offtake, and a realistic line of sight to downstream partners.

Early participation in credible exploration sits at the intersection of natural resources and future technology. The upside is real, but it accrues to investors who treat the sector with patience and read the region with care.